The Lifestyle Era: Luxury’s Opportunity in Home and Hospitality

BoF’s guide to why and how fashion and beauty brands are expanding into lifestyle — from home to dining to hotels — to extend their brand universes, deepen customer touchpoints and find new avenues of growth.

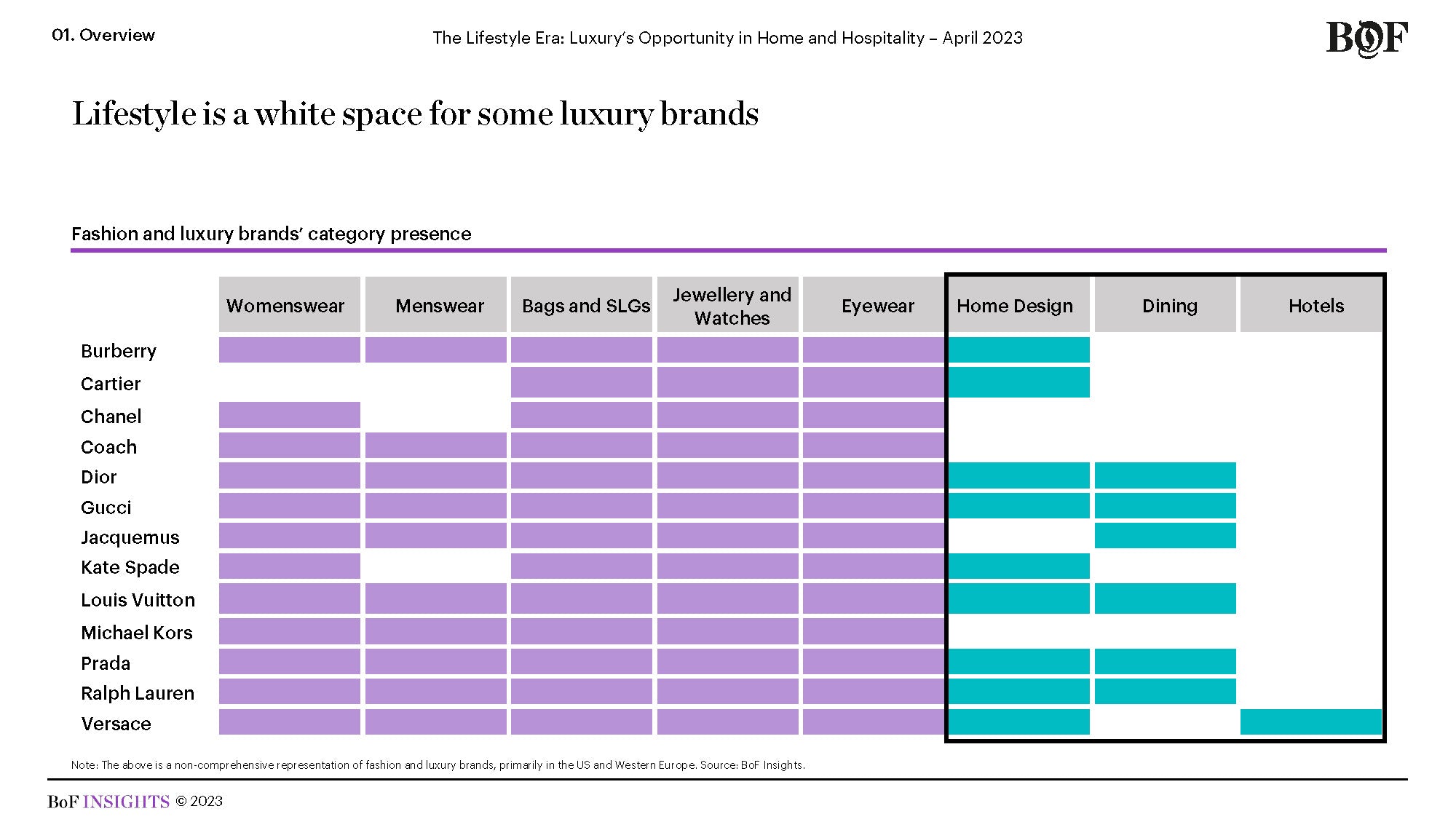

The $4.3 trillion lifestyle sector, which includes everything from homeware to hotels, may not present a new opportunity for fashion and beauty brands — after all, brands like Ralph Lauren have had home businesses brands like Armani hotels for decades now.

But what is new is the momentum such expansions are gaining, particularly since the Covid-19 pandemic led consumers to place greater importance on the spaces in which they live, work and socialise.

Fashion and beauty brands are betting on home design, dining and hospitality to not only open new revenue streams but also extend customer touchpoints and build greater brand affinity.

In ‘The Lifestyle Era: Luxury's Opportunity in Home and Hospitality,’ BoF Insights explores how and why consumer behaviour is changing when it comes to lifestyle. BoF Insights also provides a framework for how fashion and beauty brands can invest in lifestyle categories and prioritise the right tactics to reach their desired target audiences. The report is informed by almost 30 executive interviews, proprietary consumer surveys and market sizing and growth data from Euromonitor International and Earnest Analytics.

Length: 90 pages File Format: PDF

Price:

£2,495.00

Table of Contents

Timeline of Key Phases of Branded Lifestyle Offerings

Impact of Lifestyle Extensions on Brand Image for HNWIs

US Annual Spending on Home Design, Apparel and Footwear by Age

Timeline of Luxury and Fashion Brands’ First Home Design Launch

Key Operational Considerations and Consumer Trends Defining What’s Next for Lifestyle

Historic and Forecast Home Design, Hotels and Dining Market Growth to 2026

Breakdown of Home Design Subcategory Growth to 2026

Preferred Categories to Spend on for HNWIs

Comparison of Pre-Pandemic and Current Spend by Category for HNWIs in the US, UK, and France

Share of HNWIs Engaged in Branded Home Design, Dining or Hotels in the US, UK and France

Home Design Potential Share of Overall Brand Revenue

Potential to Cross-sell Home Design for HNWIs

HNWI Interest in Home Design Sub-Categories

How Brands Extend House Codes to New Categories

Case Study: Marimekko Leverages Design Concepts for Fashion and Home

Competitive Mapping of Mass, Premium and Luxury Home Design

Case Study: Fendi Targets Distinct Customer Bases Through Separate Lifestyle Offerings

Role of Interior Designers in Home Design Sales

Four Dynamics Redefining Customer Demand for Lifestyle

HNWI Key Reasons for Shopping for Home Goods

HNWI Motivations for Purchasing Fashion-Branded Lifestyle Products or Experiences

HNWI Intent to Spend on Home Sub-Categories in Upcoming Year

HNWI’s Favourite Stylistic Traits for Fashion and Home

Proportion of Fashion-Branded vs Overall Home Design Spend for HNWIs

Top Fashion and Beauty Companies for Branded Home Design for HNWIs in the US, UK and France

Qualities of Brands HNWIs are Most Interested in Purchasing Lifestyle Products From

Historic and Forecast Global Luxury Fashion-Branded Dining Sales Growth to 2026

Impact of Dining at Branded Cafe or Restaurant on Purchasing Behavior for HNWIs

Case Study: Prada and Tiffany & Co. Dining Ventures Mix Interior Design with Pop Culture

Case Study: Café Kitsuné Takes its Own Trajectory from Maison Kitsuné

Historic and Forecast Hotel Revenue Growth by Sub-Category to 2026

Impact of Staying in a Fashion-Branded Hotel on Purchasing Behavior for HNWIs

Case Study: Bulgari’s Successful Diversification into Hotel Empire

Case Study: Boucheron’s Private Apartments Treat VIPs

Case Study: Real Estate Development is Next Frontier for Brands

Three Stages of Brand Investment for a Lifestyle Offering

Luxury Fashion Brands’ Home Offerings by Sub-Category

Case Study: Louis Vuittion Extends Brand Codes Across Lifestyle Categories to Cross-Sell to Customers

Key Questions for Brands to Ask Before Investment in Lifestyle

Tactical List of Incremental Operational Steps to Expand into Lifestyle

Investment Model Balances Intimacy with Resources and Risk Appetite

Why Buy this Report

Analyses the opportunity for fashion and beauty brands to expand into lifestyle, through homeware, dining and hotels

Unpacks how cultural shifts are redefining customer attraction to lifestyle products and experiences and explains how brands can craft a long-term lifestyle strategy

Features proprietary research with high-net-worth consumers in the US, UK and France, revealing attitudes towards fashion brand extensions into home and hospitality, purchase drivers, and the most in-demand product categories and brands

Showcases perspectives from executives and industry leaders on brand extensions into home design and hospitality, including creative development, the competitive landscape and operating models

Includes concise case studies on Boucheron, Bulgari, Café Kitsuné, Diesel, Dolce & Gabbana, Elie Saab, Fendi, Louis Vuitton, Marimekko, Prada and Tiffany & Co

Research Inputs

Three panels, conducted by Altiant LuxuryOpinions® on behalf of BoF Insights, of HNWIs in the US, UK and France who each have investable assets with a median value of between $1.5 million and $2 million

28 interviews with founders, CEOs and other senior executives from fashion, beauty, home design brands and retailers, hospitality companies, as well as consultants and analysts

Market-sizing data from Euromonitor International, a global market research firm

Featured companies include but are not limited to: Anya Hindmarch, Armani, Boucheron, Bottega Veneta, Brunello Cucinelli, Bulgari, Burberry, Cartier, Chanel, Café Kitsune, Coach, Dior, Diesel, Dolce & Gabbana, Elie Saab, Fendi, Gucci, H&M, Hermès, Issey Miyake, Jo Malone, Kate Spade, Louis Vuitton, Marimekko, Missoni, Prada, Ralph Lauren, Roche Bobois, Saint Laurent, Tiffany & Co, Versace and Zara